The following chart list each of the tax planning items that are important to the Foreign Investor. Each item will be discussed together with an explanation of the disclosures and potential U.S. estate tax, U.S. gift tax, U.S. income tax, U.S. capital gains tax, U.S. Branch Tax that might apply to a Foreign Investor in U.S. real estate.

The U.S. Corporation Investment Entity

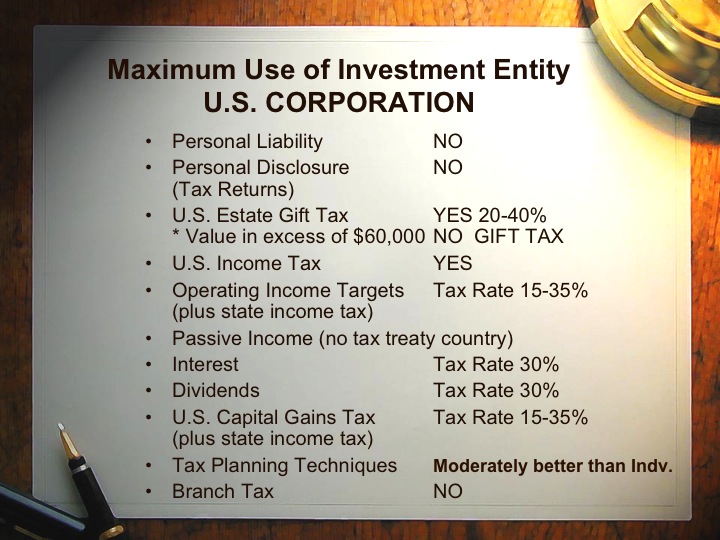

A Foreign Investor’s ownership of the share of a U.S. corporation that invests in U.S. real estate will provide that there is no personal liability on the Foreign Investor nor a requirement of filing a personal U.S. tax return. The corporation will be filing a tax return on the income earned by the corporation.

It is important to note that the shares of the U.S. Corporation are subject to the estate tax, if the individual owner of the shares dies. However, the shares of a U.S. corporation can be transferred free of a U.S. gift tax during the shareholder’s life.

The U.S. corporate income tax for U.S. corporations ranges from 15% to 35% on the corporation’s net taxable income.

Often there may be a much smaller income tax to the State in which the corporation is incorporated. The state tax is deductible from the federal income tax.

Non-recourse debt on U.S. property will reduce the value of the real estate for estate tax purposes. This results only in the net value of the U.S. real estate, (net of the debt), to be included in a U.S. real estate.

Any dividend income received by the Shareholder from corporate profits could be taxable at an additional 30% in addition to the tax on the operating income paid by the U.S. Corporation. Interest income paid to a Foreign Shareholder from a U.S. corporation is also generally taxed at 30%.

The rate of tax resulting in capital gain earned by a U.S. corporation does not provide the foreign investor with any the tax benefits from sales from gains from sales of property. It is assumed that all corporations, unlike individual investors, are in business to earn income and all of a corporation’s income should be taxed the same whether it is ordinary income or a capital gain.

No Branch Tax is applied to a U.S. corporation.

Have a question about United States Taxation of Foreign Investors? Ask Richard S. Lehman, Esq.:

")