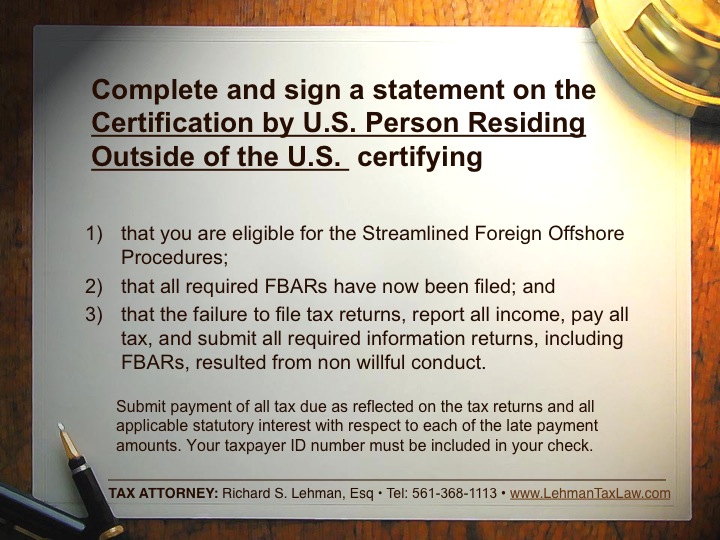

Eligibility for the Streamlined Foreign Offshore Procedures

For the most part Taxpayer’s residing outside of the U.S. will have the same requirement as those residents in the U.S. However, there are certain differences.

Taxpayers must meet the applicable non-residency requirements; and

have failed to report the income from a foreign financial asset and pay tax as required by U.S. law, and may have failed to file an FBAR with respect to a foreign financial account, and such failures resulted from non willful conduct.

Individual U.S. citizens or lawful permanent residents, or estate of U.S. citizens or lawful permanent residents will meet the applicable non residency requirement if, in any one or more of the most recent three years for which the U.S. tax return due date (or properly applied for extended due date) has passed, the individual did not have a return due date (or properly applied for extended due date) has passed, the individual did not have a U.S. abode and the individual was physically outside the United states for at least 330 full days.

")